Conventional Loan Credit Score Requirements Explained

Grasping the nuances of conventional loan credit score requirements stands as a vital phase when you prepare for homeownership. Your specific rating impacts your chances for approval plus your interest rate and the total affordability of the house. For those collaborating with Fyzl Group Ltd, knowing how banks weigh credit can be the deciding factor between a yes or a no in the tight mortgage market of 2026.

A conventional loan remains a top choice for financing a home though it involves stricter standards than government options. Throughout 2026 lenders are looking deeper into credit history plus income stability and general financial habits when they evaluate potential borrowers.

Minimum Credit Score for Conventional Loan

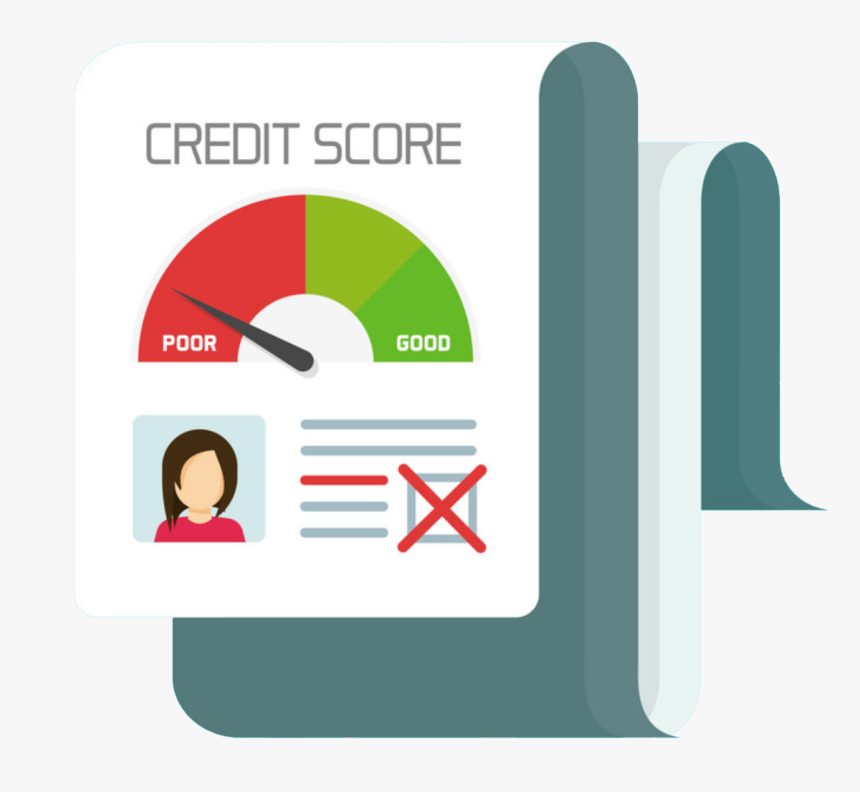

The minimum credit score for conventional loan entry usually sits around 620 but most banks want to see much higher numbers to offer you better terms.

People with a rating near 740 or higher generally get the most attractive interest rates and more relaxed approval rules. While 620 might get you through the door it often carries bigger costs and more rigid demands.

This highlights why focusing on strong credit health is a necessary move before you ever apply.

Credit Score Needed for Mortgage Approval

The actual credit score needed for mortgage approval will vary based on the lender plus the loan size and your unique financial profile.

Better credit scores prove to lenders that you carry less risk which naturally boosts your approval odds. Lower ratings might still work but they often call for a higher income or a much smaller debt load or perhaps a bigger down payment.

Your score is almost always the very first detail a lender looks at during the initial application phase.

Conventional Mortgage Requirements 2026

The conventional mortgage requirements 2026 involve several critical pillars that go far beyond just looking at a single number on a screen.

Banks look at your income stability plus employment history plus your debt to income ratio and overall savings. Having a great score paired with a steady paycheck will make the entire approval process go much faster.

These rules exist to make sure that homeowners can stay on top of their long term mortgage obligations without struggling.

Home Loan Credit Score Guidelines

Home loan credit score guidelines are used by financial institutions to sort potential borrowers into various risk categories.

High ratings usually unlock lower interest rates and smoother loan conditions while lower scores might pass only with tighter rules and added expenses.

Learning these guidelines early on helps you get fully prepared before you sit down to officially apply.

FICO Score for Home Loans

The FICO score for home loans is the industry standard used by nearly every major mortgage lender in the country.

It takes a close look at your payment history plus credit usage plus account age and the mix of accounts you currently have. Each of these pieces determines your eligibility and how much house you can actually afford.

Lenders count on FICO data to decide if a borrower is reliable enough for a massive loan.

Credit Requirements for House Loan

The credit requirements for house loan approval change slightly based on the type of house and the individual bank policies.

Conventional loans usually demand a cleaner credit profile than an FHA loan or other government products. Having excellent credit makes you a more attractive applicant and drops your total borrowing expenses.

Conventional Loan vs FHA Loan Credit Score

The conventional loan vs FHA loan credit score comparison is a big deal for buyers who are stuck between different financing paths.

Conventional options generally require a higher rating while FHA programs are famous for being more forgiving with lower scores. However you should know that FHA loans might come with extra insurance fees that stick around.

The right choice always depends on your specific financial situation and what you want to achieve long term.

FHA vs Conventional Mortgage Requirements

The FHA vs conventional mortgage requirements differ quite a bit when you look at credit flexibility and your required down payment.

FHA products are built for people with lower credit while conventional mortgages reward those with strong scores by offering lower rates and fewer hoops.

Knowing the pros and cons of both will help you pick the most affordable way forward for your family.

Best Loan Type for Good Credit Score

The best loan type for good credit score holders is almost always going to be a conventional mortgage.

A high rating opens the door to lower interest rates plus smaller monthly bills and much better terms overall. This ensures your home purchase stays cost effective as the years go by.

Great credit essentially gives you more power to negotiate with your lender for a better deal.

Low Credit vs High Credit Mortgage Options

When you look at low credit vs high credit mortgage options the gap in total cost is truly massive.

Borrowers with lower scores might fit into FHA or other niche programs while those with high scores get the perks of conventional financing.

Your credit rating does not just decide if you get the house but it dictates the total price you pay for it.

Mortgage Programs Comparison 2026

A mortgage programs comparison 2026 will include everything from conventional and FHA to VA loans and other specialized tools.

Each individual path has its own set of rules for scores plus down payments and how the interest rates are structured.

Picking the right one is about looking at your financial stability and where you see yourself in ten years.

Government vs Conventional Loans

The government vs conventional loans debate highlights the difference between public backing and private sector flexibility.

Government loans are great for supporting people who are still building their credit while conventional loans are the prize for those with established records.

A conventional loan usually saves you more money over time if you have the credit to qualify.

Conventional Loan Interest Rates

The conventional loan interest rates you see are tied directly to your score plus the current market and lender choices.

Top tier scores usually get you the lowest possible rates which keeps more money in your pocket every single month.

Even a tiny difference in your rate can change the total amount you pay back by thousands of dollars.

Mortgage Rate Based on Credit Score

The mortgage rate based on credit score will shift significantly as you move up through the different credit tiers.

People with excellent ratings get the best deals while those on the lower end face much higher costs to borrow the same amount.

This is exactly why many people spend a few months boosting their score before they start house hunting.

How Credit Score Affects Interest Rate

Seeing how credit score affects interest rate is a real eye opener for most first time home buyers.

A high score makes a lender feel safe which leads to a lower rate and better terms for the life of the loan.

Conversely a low score means the lender sees more risk and they charge you more to cover that exposure.

Lower Interest Home Loans Good Credit

Getting lower interest home loans good credit status is a huge win that provides massive financial advantages for years.

Excellent credit simplifies the process and unlocks better deals plus smaller monthly payments and serious long term savings.

This makes credit management a central part of any smart home buying strategy in today’s world.

Loan Cost Difference Credit Score Impact

The loan cost difference credit score impact can be staggering when you calculate it over a full thirty year term.

Moving your score up just a few points can sometimes save you the price of a luxury car in interest alone.

This makes keeping a close eye on your credit report a top priority for anyone serious about buying a home.

Monthly Mortgage Payment Calculation

The monthly mortgage payment calculation relies on the loan total plus interest rates plus property taxes and home insurance.

Your credit score plays a hidden role here because it determines the interest rate used in that specific math.

Having a better score simply leads to a lower monthly bill and more freedom in your budget.

Factors Affecting Mortgage Approval

Several factors affecting mortgage approval include your score plus income stability plus job history plus debt levels and cash savings.

Lenders look at your entire financial life before they decide to hand over the keys to a new property.

Maintaining a healthy financial profile across the board is the best way to ensure you get a yes.

Employment History Loan Approval

Your employment history loan approval status is a big piece of the puzzle for every mortgage underwriter.

Holding a steady job proves you have a reliable stream of cash coming in to pay for the house every month.

If you have changed jobs recently you might just need to provide a few more documents to explain the transition.

Income Stability Mortgage Requirements

Meeting the income stability mortgage requirements means showing the bank that you can handle the payments for the long haul.

Lenders like to see a consistent pay history rather than earnings that jump all over the place from month to month.

This creates a sense of confidence that the loan will be repaid on time and in full.

Credit History Importance Home Loan

The credit history importance home loan relationship is something that simply cannot be ignored or downplayed.

A clean track record shows you are a responsible borrower and it builds a bridge of trust between you and the bank.

Avoiding missed payments or big defaults is the best way to keep your home buying dreams on track.

Bank Underwriting Process Explained

The bank underwriting process explained is basically a deep dive into your financial records by an expert.

Underwriters double check your income plus credit plus debts and assets to make sure everything looks perfect.

This is the final hurdle you have to clear before you are officially approved to buy your home.

Loan Approval Checklist

A solid loan approval checklist usually starts with a credit check plus income proof plus job history plus debt analysis and asset review.

Checking off every item on this list correctly is what leads to a successful and stress free closing day.

Conclusion

Getting a grip on conventional loan credit score requirements is a must for anyone looking to enter the market in 2026. Your score is the heart of the deal because it sets the tone for your interest rate and total loan cost. If you prepare your finances early you will find much better terms and a smoother path to owning your home.

Fyzl Group Ltd knows that strong credit health plus a steady income and smart planning are the keys to a great homeownership experience.

FAQs

What is the minimum credit score for a conventional loan

Most banks look for at least 620 though you will find much better deals if your score is higher.

Is conventional loan better than FHA loan

It really depends on your score as conventional options are usually the winner for those with strong credit.

How does credit score affect mortgage interest rate

A higher score signals less risk which allows lenders to offer you a lower interest rate.

What credit score is best for home loans

Hitting a score of 740 or above is typically the sweet spot for the best rates and terms.